By Ayele Gelan (PhD)

Addis Abeba – In pursuit of its primary objective of maintaining low and stable inflation, the National Bank of Ethiopia (NBE) recently declared a shift to an interest rate-based monetary policy regime.

Under this new policy framework, the NBE will utilize its policy interest rate—designated as the National Bank Rate (NBR)—as the principal mechanism for signaling its policy stance and influencing broader monetary and credit conditions.

According to the central bank, the initial policy interest rate is set at 15%. However, the NBR will be adjusted upwards or downwards based on prevailing inflationary and monetary conditions.

Upon reviewing the two-page press statement issued by the NBE, several questions arose in my mind.

These include: Is there any evidence base informing the NBE’s latest monetary policy? Does the new monetary policy accurately reflect Ethiopia’s current economic reality? And is the 15% base rate truly appropriate for Ethiopia?

This commentary seeks to address these pertinent inquiries and provide a nuanced analysis of the NBE’s policy shift.

Evidence-base?

There is an established tradition in Ethiopia, particularly with the NBE, to formulate and present bold policy statements without making any attempt to justify them with some background studies.

Economic policy formulation is normally preceded by some background study conducted by experts. Such studies are then internally translated into the so-called white papers, rigorously prepared documents that declare policy intentions and arouse debates. Only after passing through these stages are policymakers supposed to release policy statements.

Every time the NBE introduces new policies, I skim through the NBE’s website, desperately searching for some background papers, often to no avail. The latest monetary policy is no exception.

Without a proper assessment of the situation on the ground, there is no magic through which NBE can establish the facts.

The excess money supply may not necessarily be the only cause of inflation in Ethiopia. The base rate NBE chose, 15%, may not have been set at a suitable level (these are discussed in detail further below).

The NBE has been creating the perception that it is emerging as an independent monetary authority. If NBE wishes to transform that perception into reality, then it must radically change its modus operandi.

Strengthening the evidence base for monetary policy is an indispensable feature of an independent monetary authority. This requires the establishment of a Monetary Policy Committee, consisting of some senior staff of the NBE and external researchers and policy practitioners with solid track records in the field of macroeconomics.

In the NBE governance structure, I find a list of top government officials as advisors, but with all due respect, none of them seem to have any solid background in macro or monetary economic analysis.

Macroeconomic policymaking is a team effort among highly specialized experts in the field. Therefore, NBE can redress its shortcomings in formulating evidence-based monetary policy by enhancing its capacity, essentially by establishing a monetary policy committee involving Ethiopian economists with solid expertise in the field.

Strengthening the evidence base for monetary policy is an indispensable feature of an independent monetary authority.”

Given there is no evidence base, as far as I know, accompanying the latest NBE policy statement, I will now resort to constructing and building some logic in the context of Ethiopia’s monetary policy.

Understanding how money supply leads to inflation

Money supply can lead to inflation if the following conditions are met:

The first condition occurs when authorities increase the money supply and introduce it into circulation. This expansion of credit is a deliberate policy action intended to encourage investment, create jobs, raise incomes, and improve standards of living. Authorities promote investment by lowering interest rates, making borrowing cheaper for investors, and thereby encouraging economic activity.

The second condition arises when the majority of bank loans are directed towards the private sector, which creates jobs, utilizes land and other natural resources, and produces goods and services. As a result, economic growth accelerates year on year over several cycles—for instance, over half a decade.

The third condition occurs when the rate of economic expansion and GDP growth eventually slows. This slowdown happens as the economy approaches its full potential, with nearly the entire workforce employed and most factories operating at full capacity. In other words, the unemployment rate falls to less than 5%, the so-called natural unemployment rate, which reflects the normal level of unemployment at any given time due to people transitioning between jobs.

If all three conditions are fulfilled, then additional money logically ends up causing inflation. If the third stage is reached, additional money and credit will not lead to an increase in production because there is no idle resource waiting to be employed. In other words, inflation essentially means additional money with no additional output.

When the economy reaches the end of the third stage, the authorities get signals that the economy is overheating. These signals prompt the monetary authorities to shift their priority to controlling inflation. This can be accomplished by increasing the interest rate to discourage further investment and, hence, stop the process of the economy overheating.

Traditionally, monetary authorities used the interest rate as an instrument to reconcile tradeoffs between the unemployment rate and the inflation rate. During economic downturns, the interest rate is reduced to encourage investment, create jobs, and lower the unemployment rate.

During economic booms, the interest rate is increased to discourage investment, stop the economy from overheating, and reduce the inflation rate.

In more recent decades, a series of economic shocks to the global economy, such as the recurring oil shocks, have created a phenomenon known as stagflation. This means that economic stagnation (e.g., high unemployment) and inflation began to coexist in an economy. This change has caused some complications in the formulation of monetary policies.

Regardless, monetary authorities continued to employ interest rates as effective policy instruments to mediate inflation and unemployment rates. For instance, the financial crisis of 2008–2010 has caused considerable damage to the world economy, particularly those of the developed countries, notably the USA and Europe. This caused economic slowdowns and high unemployment, which persisted during the following decade. To encourage investment and reduce unemployment, the monetary authorities reduced interest rates to near zero in those countries.

When the coronavirus pandemic hit the world, the economic slowdown worsened. By then, the interest rate had become a blunt instrument; it was already too low, and there was no room for reducing it any further! Hence, the monetary authorities devised a new instrument, quantitative easing, meaning essentially pumping trillions of additional monies into the economy without necessarily utilizing interest rates as an instrument. This had to be done to protect the welfare of their citizens, safeguard jobs, and help the survival of businesses.

Their policies worked. From 2022 onwards, just two years after the devastating pandemic, the western countries began to experience economic upturns, with unemployment rates falling close to the natural rate in most developed countries. Then the monetary authorities shifted their priorities to controlling inflation and, hence, began to raise interest rates.

For instance, the unemployment rate in the US economy progressively fell from 13.2% (May 2020) to 4% (May 2024), and the interest rate has been increased in a series of steps from 0.09% (December 2020) to 5.33% (December 2023).

Ethiopia’s inflation puzzle

When it comes to Ethiopia, the money supply has indeed increased, but this is only one of the conditions (the first condition). The governments have continuously printed and pumped huge quantities of birr into the economy for an extended period, at least for over two decades.

However, the increase in money supply has not been accompanied by credit expansion that encouraged the private sector to borrow and create jobs to the required extent (second condition). Rampant unemployment still exists, particularly youth unemployment among university graduates, which currently exists at well over 40%.

Where did the money go? Why does Ethiopia’s money supply not create jobs in the productive sectors and hence reduce inflation?

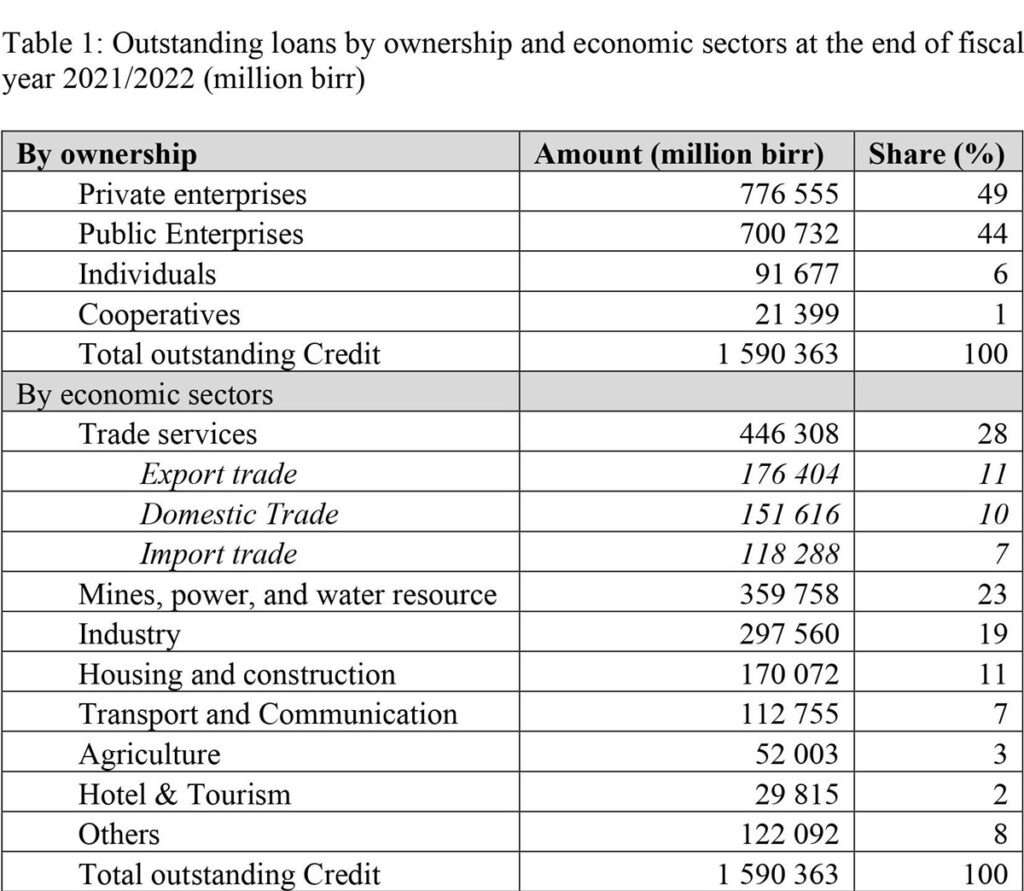

I would like to illustrate this point by relying on Table 1, which is constructed from data obtained from the NBE website. The table presents a summary of outstanding loans at the end of 2021/2022. A total of 1.6 trillion birr was registered as an outstanding loan during this period.

The upper part of the table presents the figures in terms of public and private sector shares in total loans. The share of private enterprises was 49%, while that of public enterprises was 44%. The fact that public enterprises have had about the same amount of total loan has profoundly serious economic implications.

If the share of private enterprises was relatively larger, then more goods would have been produced and supplied to the domestic market. Public enterprises are unlikely to produce goods that would appear on supermarket shelves.

Now I turn to the lower part of the table: the allocation of the outstanding loans by economic sectors, ranked from the largest to the lowest in their shares of total outstanding loans. The trade and distribution sector comes on top with 28%.

Export trade and import trade received 11%, 10%, and 7%, respectively. Mining, power, and water resources come in second with 23%. The share of the industrial sector was 19%. This share is likely to be influenced by large enterprises and their capital expenditure on infrastructure, e.g., industrial parks.

The share of small and medium-sized enterprises responsible for producing goods and supplying them to markets is likely to constitute a negligible proportion of the share of the industrial sector.

The agricultural sector has a shockingly low share of 3% of the total outstanding loans.

Evidently, the money supply has been funneled into the Ethiopian economy through sectors that have no direct contribution to the production of goods that will appear in markets. The fact that only 3% of total loans went to the agricultural sector explains the situation very well.

It should be noted that expenditure on food products has the largest weight in a typical Ethiopian household budget.

The banking sector provided such a negligible loan to agriculture and manufacturing (productive sectors that supply goods to the market), and they have pumped considerably large sums of money to the not-so-productive public and private sectors that undertake investment projects, create jobs, and pay wages and services, contributing to increasing demand for goods and services in the markets.

Ethiopia’s inflation can be explained by the ever-widening gap between demand for goods and supply in the domestic market. The banking sector has inadvertently engineered the creation and worsening of this imbalance.

They contributed to the scarcity of goods by not providing loans to productive sectors, and they have enhanced the expansion of demand for goods and services by generously lending to non-productive sectors.

Market power

Market power is a major determinant of access to bank loans in Ethiopia. The exceptionally high lending interest rate plays a critical role in this process. The fact that the cost of borrowing is excessively high does not stand in the way of crony businesses that have considerable market power. Most producers in the non-agricultural sectors of Ethiopia, particularly large businesses, have a degree of market power.

For instance, it is not surprising that those engaged in import and export businesses have amassed disproportionately large shares in total bank loans. They would not hesitate to borrow even at 20% or more interest rates because they use their market power to pass on costs they have incurred onto buyers of their products. After all, Ethiopia has sellers’ markets in most non-agricultural sectors.

It should be noted that Ethiopia’s import sector is dominated by oligopolistic businesses, who tacitly agree among each other to fix prices, often adding 100% to 400% margins to products they import. Critically, when importers charge consumer prices with shockingly high margins, including passing on the high cost of bank interest rates to buyers, this aggravates the country’s inflation.

Producers that do not have market power have no capacity to pass on the high interest rate to buyers of their products. Farmers and small and medium-sized manufacturing enterprises do not have market power; after all, there are millions of such businesses, and hence they compete among themselves, charging competitive prices. An excessively high interest rate is not the kind of cost that small producers can afford to absorb either.

That is why farmers and SMEs are effectively excluded from bank loans in Ethiopia. It is not that banks turn down their applications for loans. Affordability is the issue here. Small producers exclude themselves from the credit market because they know that, at the prevailing lending rates, they cannot borrow and become profitable.

Critically, in this manner, the unaffordable high lending rate effectively serves as a barrier to entry for millions of small producers, excluding millions of farmers and small producers from accessing the existing bank loan facilities.

Even if the lending interest rate is sufficiently lowered, farmers would still encounter yet another hurdle: bank collateral! Smallholders have extremely loose entitlement to agricultural land because land in Ethiopia is owned by the state. This means that in the current situation, farmers cannot use the land as collateral for bank loans.

Essential insights

There is a perception that Ethiopia’s inflation has been caused by increases in the money supply. The authorities at the NBE seem to subscribe to this viewpoint, partly being pressured by the IMF, which often blames inflation on excessive money printing by governments in developing countries.

In this piece, I have established that the claim that the money supply has caused Ethiopia’s inflation can only be partly valid. It is indeed the case that the authorities have been printing huge quantities of money and putting them into circulation. This has happened for an extended period of time, at least for two decades. However, a considerably large proportion of the money printed has been used by the government to finance unproductive expenditures, including capital expenditure on mega projects and ordinary expenditure on salaries of civil servants employed in the bloated public sector.

A disproportionately large share of the loans has been allocated to the private sector, which does not produce goods that would not end up on supermarket shelves. For instance, import and export trade have continuously received a large proportion of loans, but these do not produce goods; rather, they distribute what has already been produced in the domestic economy, or else import foreign produce, add exorbitant margins, and sell in domestic markets, fueling inflation.

The bottom line is that the credit expansion has not created jobs in productive sectors such as agriculture and small and medium-sized manufacturing enterprises. The current unemployment rate in Ethiopia is considerably high.

The shortcomings of the latest NBE monetary policy can be categorized into two broad groups. First, the policy formulation was not informed by any evidence base. The NBE should redress this shortcoming by establishing a monetary committee, which will need to bring together Ethiopian expertise with good track records in macroeconomics.

Second, the new macroeconomic policy is simply out of touch with the reality on the ground in the economy of Ethiopia. Ethiopia has considerably large idle human and natural resources. In this circumstance, monetary policy is expected to reduce inflation by enhancing the production of goods and services and relaxing supply constraints.

The NBE should practice the normal central bank function of appropriately using the interest rate as an effective instrument to mediate unemployment and inflation. Given the exceptionally high unemployment rate, NBE should immediately shift to a low interest rate regime.

It defies logic that the NBE fixed the base rate at such a high rate, 15%, with so many idle human and natural resources. The NBE should promptly reduce the base interest rate to a lower single digit, say 5%, and instruct commercial banks to lend at no more than 8%.

A low interest rate will attract millions of small businesses, which means a huge increase in the customer base, and hence the banking sector will make considerably larger profits. Their loss from charging lower interest rates will be more than compensated by gains from large volumes of loans.

The interest rate reform should be accompanied by targeted lending, giving priority to productive sectors such as agriculture and manufacturing enterprises. AS

Editor’s Note: Ayele Gelan (Ph.D.) is a research economist working at the Kuwait Institute for Scientific Research (KISR). He researches, studies, and shares perspectives on economic modeling and practices on Ethiopia, Kuwait, and Scotland. He tweets at @AyeleGelan.