Analysis: How Can Ethiopia Boost Remittance Inflows?

Ayele Gelan, (PhD), For Addis Standard

Addis Abeba, July 24/ 2018 – Ethiopia has been in a dire state of foreign exchange crisis for the last few years. PM Abiy has made a plea to the Ethiopian diaspora to come to the rescue of their country by sending hard currencies back home. In this piece I will assess gaps between actual and potential inflows and then explore options to boost remittances.

Figures

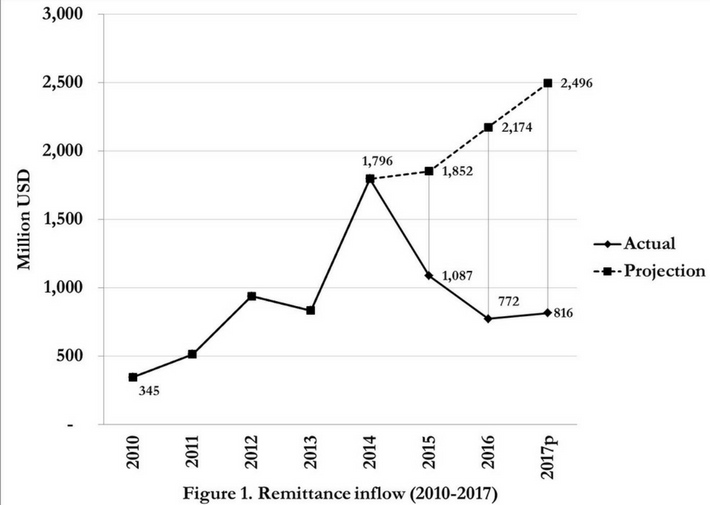

The data plotted in the Figure 1 was obtained from the World Bank migration and remittances database, It shows the dynamics of remittances during 2010 to 2017. Remittance inflow was only US$345 million in 2010 but it sharply rose to US$1,796 million in 2014, and then plummeted to US$816 million in 2017, about 45% of the peak reached in 2014.

2014 was the year Oromo Protests was ignited in Ambo, spread to the rest of Oromia like a forest fire, and finally engulfed the whole nation, when Amhara Resistance followed suit. A relentless campaign ended up with a remittance boycott to punish the regime that desperately needed hard currency to sustain itself and stay on power.

In Figure 1, the solid line shows a plot of actual remittance inflows, but the dotted line projects the 2010 to 2014 trend up to 2017, that is to say what would have happened if the remittance boycott did not take place. The gaps between the solid and dotted lines indicate the amount remittance inflow that remained unrealized due to the remittance boycott.

Remittance inflow would have reached US$2,496 million by 2017 if the situation stayed normal. Ethiopia lost remittance inflows amounting to US$765 million in 2015, US$1,402 million in 2016, and US$1,681 in 2017. The losses over the three years period amounted to US$3,847 that is to day Ethiopia lost nearly US$4 billion of remittance inflows during that period.

Facts

There are gaps between figures and facts as far as remittance inflow to Ethiopia is concerned. The World Bank estimates seem to grossly underestimate the facts on the ground. I would adduce two pieces of evidences.

Firstly, in the World Bank database, remittance figures are very closely related to stock of migrants, that is the total number of migrant outflows from that country over several years. The number of Ethiopian migrants living in most countries tends to be under reported. It follows that remittances to Ethiopia from most country is underestimated.

Let’s take the case of Kuwait, a country whose situation I know closely. In the World Bank database, the number of Ethiopian migrants living and working in Kuwait and the amount of remittance in 2017 were given as 3,917 and US$5 million respectively. However, official statistics in Kuwait indicates that there are at least 74,000 Ethiopians living and working in Kuwait. If we apply remittance per migrant in the World Bank estimates to the latter figure then the amount of remittance from Kuwait would rise from US$5 million to US$94 million. The case of Kuwait could be rather extreme but certainly unlikely to be an isolated one.

Secondly, as I have reported in another piece, remittances to Ethiopia tend to get underestimated for many other reasons. Sizeable gaps have always existed between Ethiopia’s the official and the parallel currency exchange markets. For this reason, substantial sum of remittance transfers have taken place through informal channels. In order to get better rates and also avoid transfer fees, Ethiopians in diaspora choose to carry hard currencies with them and then directly exchange it to birr in local underground markets. Alternatively, they commonly send hard currencies via friends or any traveller they would trust. The World Bank estimated that 14% of Ethiopians to whom money was transferred from abroad in 2010 got it through travelers. The other dimension of informal transfer is the case of hard currency remaining abroad because of a more sophisticated black market operators who act pretty much like the way foreign money transfer services.

Stocktaking

The figures and facts discussed in the preceding sections can serve as a stocktaking exercise. The remittance boycott might have had unfortunate consequences on the economy but it also provided the authorities with excellent insights that the diaspora communities have extraordinarily capacity to quickly adjust remittance inflows depending on circumstances.

The boycott campaign was a call not to send money through official channels. It was a negative shock, deliberately so to hurt the regime at the time. PM Abiy’s recent plea can be seen as a positive stimulus to inspire the diaspora community to come to the rescue of their motherland, alleviating the nation from the ongoing foreign exchange crisis. Given PM Abiy’s goodwill and positive image among all sections of Ethiopians, both at home and abroad, I have no doubt the setback in the remittance inflow would be very quickly reversed and the hard currency inflow would buck up to its previoustrend in the near future.

How soon this can happen will depend on how proactively the monetary authorities would put the right incentives in place. The authorities can learn at least two things from the remittance boycott. First, there is a lesson on the behavior of the Ethiopian diaspora. If the diaspora have responded to a disincentive, then it follows that they can also respond to incentives as quickly and as decisively.

Second, the authorities now have a sense of magnitude, quantifiable figures with which to start planning remittance inflow targets. In response to the remittance boycott, remittance inflow deviated from the trend, causing a cumulative shortfall of about US$4 billion. It is expected a positive stimulus to remittance inflow would generate additional US$4 billion over the coming three years, one billion USD additional inflow per year. I stress that these figures would considerably underestimate the underlying facts, as stated earlier.

In a World Bank survey of 2010, remittance recipients utilized the money they received in the following proportions: 57% daily expenses, 29% university education, 9% small businesses, 4% savings and 1% housing. It seems this survey focused on money transferred exclusively for use by recipients’ relatives. However, individuals in the diaspora community do transfer sizeable funds for their own savings (e.g. domestic workers in the Middle East) as well as investments (e.g. buying or building houses). The monetary authorities would need to undertake a more thorough and comprehensive study as part of a baseline assessment to inform remittance policy design.

Anomalies

Little do the top level authorities like PM Abiy know that there are obstacles deliberately put in place to obstruct normal inflow of remittances. Who created such strange obstacles and why remains unclear. It is paramount that the authorities are aware about the existence of anomalies in Ethiopia’s remittance inflow system and undertake a thorough diagnosis with a view of removing them.

I would illustrate this using data presented in Table 1. A while back I walked into a branch of money transfer operator known as Bahrain Exchange in Kuwait. As usual, popular currencies and their daily exchange rates were listed on the board in two columns, as shown in Table 1: one rate for crediting to a bank account and another rate for cash pick-up. As it happened the Ethiopian birr was one of the popular currencies listed.

I was shocked to learn that the rate for the Ethiopian birr was the odd one out on that board. In order to make this clearer in Table 1, I have created a third column, “bank to cash (%)” by expressing the ‘credit to bank account’ as a percentage of ‘cash pick-up’. For most countries this ratio is close to 100% but for Ethiopia it is 74%.

Table 1. Ethiopia’s remittance anomaly!

| Currency | Credit to a Bank Account | Cash Pick-Up | Bank to cash (%) |

| Eritrean Nakfa | 48.35 | 48.20 | 100.32 |

| Ethiopian Birr | 66.72 | 89.87 | 74.25 |

| Egyptian Pound | 58.57 | 58.49 | 100.14 |

| Indian Rupee | 225.01 | 224.52 | 100.21 |

| Bangladesh Takka | 275.64 | 276.91 | 99.54 |

| Sri Lankan Rupee | 526.76 | 527.18 | 99.92 |

| Philippine Peso | 175.79 | 176.31 | 99.71 |

| Nepalese Rupee | 359.71 | 360.79 | 99.70 |

| Pakistani Rupee | 400.51 | 419.62 | 95.45 |

| US Dollar | 3.30 | 3.29 | 100.12 |

| British Pound | 2.50 | 2.52 | 99.33 |

Source: Bahrain Exchange Kuwait (https://www.bec.com.kw/currency-exchange-rates?atype=money&continent=popular) Money Transfer Rates per Kuwaiti Dinar (KWD) @ 10:43pm 17th Jul 2018

This implies that Ethiopian authorities have created a system that actively discriminates against transferring to bank accounts, the most convenient money transfer mechanism! Currently, if one Kuwaiti Dinar (KWD) is transferred to a bank account, only 68 birr arrives but if it is a cash pick-up, then the beneficiary would receive 90 birr, a difference of 22 birr per KWD, I found this mind-boggling, it defies logic!

I was so baffled with my encounter that I had to seek for explanation from the staff. However, they could not offer any help except to acknowledge that it was a weird stuff indeed, adding that if I insisted to send to a bank account then I could do so only if I have an account with the Commercial Bank of Ethiopia. However, cash pick-up services are available at any branch of many banks in Ethiopian including private banks. The disincentive created against transferring to a bank account must have had incalculable damages at many levels.

First, ruling out the most convenient currency transfer through official channels thereby worsening Ethiopia’s foreign exchange crisis. At least 95% of those who live in Kuwait are domestic workers, earning extremely low wages in the households sector. Their monthly earning would range somewhere between KWD 80 to 150 per month (US$260 to 490). The size of their income could be low but their saving rate is extremely high, at least around 75% of their monthly earnings! A simple calculation would establish that at the very least US$300 million would have been remitted from Kuwait annually if the situation were right. That potential remains unrealized, at least not visible in official flows.

At this juncture I would hasten to add that Ethiopian Embassies in the Middle East, who closely know the situation, have often turned a blind eye to the appalling situation. Instead of helping the hundreds of thousands domestic workers with secure way of transferring their savings through formal channels, they often add another layer of red tape, by encouraging them to come to embassies to open a bank account back home, and making initial transfer money through them.

The foreign exchange revenue lost to the Ethiopian economy is nothing compared to the incalculable damages that occurred to the lives and livelihoods of those domestic workers. The system literally forced them to use only one transfer option – cash pick-up by a family member, a relative, or a friend! More often than not, they end up losing their hard earned incomes because those entrusted with the money would end up spending it either partly or entirely.

Incentives

The authorities should aim to realize the full potential of the remittance inflows. This requires more ambitious and far reaching measures than inducing remittances to relatives back home. The most radical measure would be to encourage diaspora saving accounts in foreign currencies in the Ethiopian banking system.

(a) Saving Accounts in Foreign Currencies. As a matter of fact, there is already a policy of diaspora saving accounts in the Ethiopia. However, it seems this was never taken seriously neither by the authorities nor by the diaspora community. To be honest, the banking practice used to served it proved to be exceptionally substandard.

Here is my anecdote. I opened an dollar account and deposited a certain amount, hoping I would start a regular saving into that account. At the end of the transaction, I expected a standard document to prove that I opened and own an account. However, I was told they had not started issuing a saving book for a dollar account. I asked what evidence would I have for my deposit then. I was told I could use the receipt I was given for the deposit. It all sounded an archaic banking practice. I asked if I could talk to the manager. The manager kindly agreed to discuss the matter with me, but at the end of the day he could not offer any sound explanation. I was taken aback by the whole affair. I never bothered to top up that deposit account. Whatever I deposited I had to use as quickly as I could. The moral of this story is that a solid incentive system to attract hard currency would start with confidence building measures which would include modernizing the banking practices.

(b) Competitive and attractive interest rates for hard currency saving accounts. This measure would induce the diaspora community to choose saving more with Ethiopian domestic banks than anywhere else in the world. Fortunately, given the extremely low interest rates in most countries, only a marginal increment on top of interest rates elsewhere would induce substantial hard currency inflows.

(c) Structure interest rates based on access to the funds. It is standard banking practice that saving interest rates would depend on frequency of fund withdrawals. An instant access saving account would attract relatively smaller interest rates, although in the case of Ethiopia’s diaspora account, even this has to be reasonably high to entice more potential savers. However, saving accounts with fixed term notice periods (e.g. three months, six months, or 12 months or more) should be made available at higher rates. The existence of such longer term options would create considerable amount of hard currency pool in the Ethiopian banking system. For instance, in the worst case scenario, Ethiopia’s diaspora community has transferred around one billion USD in 2017, mostly to support relatives. If they can transfer that much to support family then they can save at least as much amount for themselves. It is the potential of attracting what is left in their foreign bank accounts, at least one billion USD being deposited in Ethiopia’s banking system every year. The cumulative stock of hard currency in Ethiopia can rise very quickly in a few years.

(d) Encouraging investment. There have often been relentless campaigns to entice the diaspora community to consider investment opportunities but, like everything else, the calls remained empty words and meaningless gestures which have never been taken seriously by everyone involved. This was so partly because of mutual distrust between the Ethiopian diaspora and the authorities. The campaign itself was more political than economic motive. Now the situation is different, the fog of mutual distrust seem to have faded away and it is high time that the authorities engage in earnest with the diaspora community and invite them to invest in their homeland. Perhaps this requires at least two sets of accompanying measures. Removing existing restrictions and exceptions with where Ethiopia’s diaspora can invest. For instance, currently the financial sector is not open to the Ethiopian diaspora community. Lifting the ban on dual citizenship is required, this is simply to acknowledge the sense of belongingness which is already in place.

(e) Recognition and prizes. These are part of the incentive mechanism. For instance, Bangladesh experienced a similar downward trend in remittance inflows a few years back. They immediately put in place measures to reverse the trend and with considerable success. Remittance inflows increased by more than 35% by October 2017. Also, they introduced a range of prizes for individual remitters in different categories, as well as banks that implemented the policies, depending on the amount of remittances they have attracted.

Challenges

Two challenges would remain. First, the incentive to open dollar saving accounts would to a certain extent divert remittances from informal to formal channels. The reason is that the hard currency would stay deposited in Ethiopia and the depositor will have the opportunity to exchange it to local currency in the future at a better official rate. The assurance of this accrued benefits as well as the attractive interest rates are expected to reduce the gap between what the remitter would get through the formal and informal channels. However, it is highly unlikely that such expected benefits would make Ethiopia’s black market in hard currencies to disappear. This is particularly the case given Ethiopia’s extremely high propensity to import goods and services from the rest of the world.

Second, paradoxically, successes in inducing remittance inflows would inevitably make the birr appreciate and hence hurt exports of goods and services, the gain through remittances would induce losses in goods markets. Incidentally, although this has not been discussed much in the past, it is this inbuilt conflicts which must have been the underlying causes of Ethiopia’s recurring devaluations during the last decade.

The combined effects of persistence in parallel currency market and adverse effects of success in attracting remittance inflows would inevitably pose a policy dilemma. However, there is nothing beyond human endeavor. Extraordinary situations require extraordinary measures. For instance, it is a common practices for a country under substantial balance of payments difficulty to resort to a dual exchange rate mechanism for a certain period of time. This would involve adopting a floating or market determined exchange rate in one market (e.g. remittances and capital inflows) and fixed or pegged exchange regime in another market (e.g. in import and export markets). This requires innovative policy-making on part of Ethiopia’s monetary authorities.

Awareness

In the past, there were awareness cum propaganda campaigns to engage with the diaspora community but accompanied with little else. Now it would prove useful to change the sequence – putting in place the right incentive structures and then engage in an extensive publicity campaign to raise awareness among the diaspora community about the opportunities created. There is no need to approach the diaspora with a plea. What needs to be done is to create conditions whereby the actions of the diaspora would amount to simultaneously helping their motherland and helping themselves.

Incidentally, PM Abiy can bring in more billions of dollars into National Bank of Ethiopia by instructing Ethiopian Embassies in the Middle East to properly do their job of facilitating remittance transfers in the simplest ways possible than by lobbying leaders of those countries to extend their helping hands. AS

ED’s Note: Ayele Gelan is an economist by training. He can be reached at augelana@gmail.com. He tweets @AyeleGelan